Blog

How Newly Arrived Immigrants in the UK Can Stay Financially Compliant

Moving to a new country involves far more than finding a place to live and starting a job. The financial obligations that come with UK residency tax reporting, HMRC registration, overseas income declarations are rarely explained during the relocation process, and most newcomers discover them only after something has gone wrong. Working with a tax accountant for foreigners who understands the specific challenges of a first-year arrival can prevent the kind of compounding problems that start small and become significant. This guide walks through what HMRC expects, what commonly catches new residents off guard, and how to build a financially compliant life in the UK from the beginning rather than trying to reconstruct one later.

Why Financial Compliance Matters from Day One?

There is a reasonable temptation, when settling into a new country, to treat tax as something to figure out later. The immediate priorities are obvious: housing, employment, banking, family. Tax feels abstract by comparison.

The problem is that HMRC’s deadlines do not adjust for how recently someone arrived. Penalties for late Self Assessment registration, missed filing deadlines, or unreported income apply regardless of whether the taxpayer knew the rules. And the consequences extend beyond financial penalties. Unresolved tax issues can create complications during visa renewals, ILR applications, mortgage approvals, and business financing requests, all things that matter considerably to someone building a new life in the UK.

Getting compliance right early, by contrast, creates a clean financial record that makes every subsequent step easier. A history of correctly filed returns, accurate NI contributions, and timely HMRC correspondence builds the kind of financial credibility that UK institutions, banks, lenders, and government agencies respond to positively.

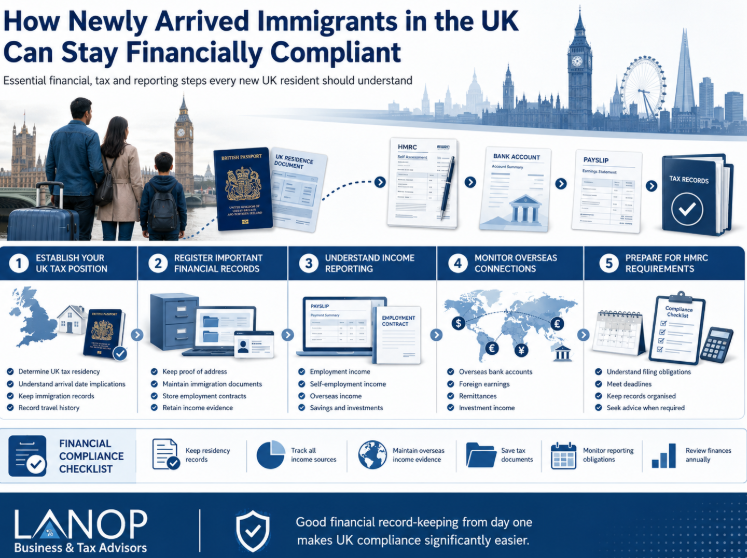

Your First 90 Days in the UK: A Financial Compliance Checklist

The first three months set the tone for your tax position going forward. A few structured steps in the right order prevent most of the problems that create work later.

Week one: Register your address with relevant services, open a UK bank account, and clarify your employment status employed, self-employed, or contractor. This distinction determines which tax obligations apply from day one.

First month: Apply for a National Insurance number through the HMRC online service. Without it, your employer cannot correctly allocate your tax contributions. Check the tax code on your first payslip. An incorrect or emergency code results in too much tax being deducted, which HMRC will eventually return but takes time to resolve. Start keeping records of all income from the arrival date.

Months two and three: Assess your tax residency status using the Statutory Residence Test. Identify all overseas income sources rental properties, savings interest, dividends, pension payments and determine whether Self Assessment registration will be required. If it is, the deadline applies from the end of the tax year in which the obligation arose, not from when you eventually discovered it.

Understanding UK Tax Residency

Tax residency and immigration status are not the same thing, and confusing the two creates real problems.

A person holding a UK work visa is not automatically a UK tax resident and equally, someone who arrived mid-year on a temporary basis may become tax resident in the UK depending on how many days they spend here and what ties they have to the country. The Statutory Residence Test is the formal mechanism HMRC uses to determine residency, and it considers day-count, employment ties, family connections, and accommodation.

One of the most persistent misconceptions is that spending fewer than 183 days in the UK makes someone non-resident. That threshold matters, but it is not the only consideration. A person with UK-based employment, a UK home, and close family here can become a tax resident even with a relatively short physical presence, depending on other factors in the test.

Moving to the UK mid-tax year introduces another layer: split-year treatment. Under this provision, the tax year is divided at the point of arrival, and UK tax obligations apply only from that date rather than the full year. It sounds straightforward, but the conditions for claiming split-year treatment are specific, and applying it incorrectly creates discrepancies in your HMRC record.

What Income Must Be Reported to HMRC?

Once a UK tax resident, the reporting obligation is broad: worldwide income. That includes employment income from a UK employer, but also salary from an overseas role, rental income from a property in another country, dividends from foreign investments, savings interest earned in an overseas bank account, and pension income arriving from abroad.

| Income Source | Usually Reportable? | Common Exception |

| UK employment salary | Yes | N/A covered by PAYE |

| Overseas employment income | Yes | Non-resident periods before arrival |

| UK bank interest | Yes | Within personal savings allowance |

| Foreign bank interest | Yes | Below de minimis thresholds in limited cases |

| Overseas rental income | Yes | Split-year period before UK arrival |

| Dividends (UK or overseas) | Yes | Within dividend allowance |

| Foreign pension income | Yes | Depends on applicable tax treaty |

The table above covers the most common categories. The honest answer to the question “do I need to report this?” is almost always yes,the question is usually whether any relief or allowance reduces the liability, not whether the reporting obligation exists at all.

Do You Need to File a Self Assessment Tax Return?

PAYE handles tax on employment income automatically. Many new arrivals assume this covers their entire tax position. It does not.

Self Assessment is required the moment any income exists outside of PAYE self-employment, freelance work, overseas rental income, foreign dividends, or savings interest above the personal allowance. It is also required for employees earning above £100,000 annually, regardless of whether PAYE has deducted tax throughout the year.

A quick decision framework: if your only income in the UK is from a single employer and you have no overseas assets or additional income streams, Self Assessment is probably not required. Add any one of the following freelance work, overseas property, foreign savings, dividend income above the annual allowance and it almost certainly is.

Registration must happen by 5 October following the end of the tax year in which the obligation arose. Filing the return is due by 31 January. Missing registration triggers a penalty. Missing the filing deadline triggers a £100 penalty automatically, with further daily charges applying after three months even when no tax is ultimately owed.

Can HMRC See Overseas Income and Foreign Bank Accounts?

This question comes up constantly, and the answer has changed significantly in recent years.

Under the Common Reporting Standard, financial institutions in over 100 countries automatically share account data with foreign tax authorities. This includes account balances, interest earned, and in some cases, transaction summaries. HMRC receives this data and cross-references it against tax returns. The assumption that overseas accounts are invisible to UK authorities is no longer safe and in many cases, is simply incorrect.

The practical implication is straightforward: reporting overseas income proactively is significantly safer than hoping HMRC does not already have the data. When HMRC raises an issue they have identified through international data sharing, the resulting investigation carries higher penalties and considerably less goodwill than a voluntary disclosure.

I Paid Tax Abroad Will I Be Taxed Again?

The anxiety around double taxation is understandable and common. The reassuring answer is that the UK has double taxation treaties with over 130 countries, specifically designed to prevent the same income from being fully taxed in both jurisdictions.

The mechanism works through foreign tax credits. If you paid tax in another country on income that is also reportable in the UK, the tax paid abroad is credited against your UK liability. The result is that you pay the higher of the two rates rather than both in full.

Three practical scenarios illustrate this clearly. An employee relocating from India who continues receiving income from an Indian employer during the overlap period can typically offset Indian tax paid against any resulting UK liability. A property owner moving from Pakistan who receives rental income from a Lahore property declares that income in the UK but receives credit for any Pakistani withholding tax already deducted. An investor relocating from South Africa with South African dividend income applies the relevant treaty to determine how much, if any, additional UK tax applies.

The treaties do not eliminate reporting obligations the income still needs to be declared. What they prevent is the full tax cost landing twice.

The Five Most Expensive Tax Mistakes New Immigrants Make

Several errors appear consistently when new residents’ tax positions are reviewed for the first time.

Assuming PAYE solves everything is the most common starting point for subsequent problems. PAYE handles employment income only; every other income stream requires separate reporting.

Ignoring overseas income because it was earned abroad or taxed there. Residency creates a worldwide income obligation that does not have a geographic boundary.

Missing Self Assessment registration deadlines often because the person did not know they needed to register until well past the 5 October deadline.

Misunderstanding tax residency and assuming visa status alone determines their position. It does not, and this misunderstanding can result in years of incorrect filings.

Failing to keep records of overseas income, foreign tax paid, and transactions during the transition period. Without documentation, legitimate reliefs and credits cannot be claimed, and HMRC queries cannot be answered.

The consequences of each: penalties starting at £100 and escalating, interest on underpaid tax, and in serious cases, formal compliance investigations that are time-consuming and stressful to resolve.

Self-Employment and Business Compliance for Immigrants

Many immigrants arrive in the UK intending to work for themselves, either as freelancers, contractors, or by starting a business. The compliance requirements here are distinct from employment.

Sole traders register with HMRC as self-employed and file annual Self Assessment returns reporting income and allowable expenses. A limited company creates a separate legal entity with its own Corporation Tax obligations, annual accounts, and Companies House filings a more complex structure that is appropriate for some situations and unnecessary overhead for others.

VAT registration becomes compulsory once taxable turnover exceeds £90,000 in a rolling twelve-month period. Below that threshold, voluntary registration is possible and sometimes advantageous, depending on the nature of the business and its customers.

Record-keeping for self-employment requires more discipline than employment. Every invoice, receipt, bank statement, and business expense needs to be retained, typically for at least five years from the Self Assessment filing deadline for the relevant year.

When Professional Tax Support Becomes Valuable?

The point at which managing a tax position alone becomes genuinely risky is usually earlier than people expect.

Overseas property, foreign investments, business income running alongside employment, multiple income streams across different countries any one of these introduces complexity that the standard HMRC guidance does not fully address. Combine two or three, and the probability of an error increases considerably.

Engaging a tax accountant for foreigners who works regularly with new UK residents means someone is looking at the full picture: residency status, overseas obligations, applicable treaties, split-year eligibility, and filing deadlines across jurisdictions. The value is not just in completing returns accurately.it is in identifying reliefs and planning opportunities that a generalist or a self-prepared return would miss.

When choosing professional support, look for demonstrated experience with international tax situations, familiarity with the Common Reporting Standard and its implications, and a clear approach to overseas income rather than a practice that primarily handles straightforward domestic returns.

Frequently Asked Questions

I have just moved to the UK and still have a bank account in my home country. Do I need to tell HMRC about it?

Not the account itself, but any income it generates. Interest earned overseas is reportable once you become a UK tax resident. Under the Common Reporting Standard, financial institutions in over 100 countries share account data with HMRC so assuming the account is invisible is no longer safe. Declare the interest on a Self Assessment return and claim credit for any foreign tax already deducted.

I worked in my home country for part of the year before moving to the UK. Do I owe UK tax on that income?

Generally no, provided split-year treatment applies. This divides the tax year at your arrival date, meaning UK tax obligations apply only from that point. Income earned before arrival falls outside the UK tax net in most cases. Split-year treatment is not automatic though specific conditions must be met, and applying it incorrectly creates discrepancies that can surface years later.

I am on a skilled worker visa does that mean I am automatically a UK tax resident?

No. Visa status and tax residency are determined separately. The Statutory Residence Test not your visa determines residency, considering days spent in the UK, employment ties, and whether you have a home here. Most people on a skilled worker visa living full-time in the UK will meet the residency test, but assuming residency based on visa status alone is a mistake that creates incorrect tax filings.

What happens if I forget to register for Self Assessment and miss the October deadline?

A penalty applies, but the situation is correctable. Registering and filing as soon as the gap is identified consistently produces a better outcome than waiting for HMRC to raise the issue. When HMRC identifies an unfiled obligation independently, the investigation carries higher penalties and considerably less flexibility than a proactive disclosure.

I am self-employed working with clients in the UK and abroad. How does that affect my tax position?

Income from both sources is reportable to HMRC once you are a UK tax resident. Double taxation treaties may provide relief where tax was already paid abroad on the same earnings. VAT registration becomes compulsory once taxable turnover exceeds £90,000 in a rolling twelve-month period, regardless of whether some turnover came from overseas clients. Keeping records separated by income source makes the annual filing considerably more straightforward.

Final Thoughts

Financial compliance in the UK is not complicated when approached from the start. What creates difficulty is delay leaving residency questions unresolved, letting overseas income go unreported, missing deadlines because the system felt unclear.

Lanop Business and Tax Advisors works with newly arrived immigrants across the UK who are managing their tax position for the first time. From confirming residency status and registering for Self Assessment, to foreign tax credits, split-year treatment, and overseas income reporting we handle the details so you can focus on settling into your new life without an unresolved tax position sitting in the background.

The foundations are straightforward when you have the right support from day one. Lanop Business and Tax Advisors is here to provide exactly that.

How Newly Arrived Immigrants in the UK Can Stay Financially Compliant

Top Health Colleges in the Middle East in 2026

What Really Happens When Pet Food Passes Its Expiry Date

How Dry and Wet Pet Food Are Made and Why Ingredients Matter

Top Health Colleges in the Middle East in 2026

Tennis Chain Durability: Diamond Setting, Structural Strength, and Long-Term Wear

3 Steps to a Successful Quinceanera

Building Stronger Communities Through Corporate Partnerships

Understanding Professional Networks for Expert Knowledge

General Audience: Key Considerations When Evaluating Ai Orchestration by Ba Insight

Christina Erika Carandini Lee: A Life of Grace, Heritage, and Privacy

Trey Kulley Majors: The Untold Story of Lee Majors’ Son

Nick Schmit? The Man Behind Jonathan Capehart Success

Jamie White-Welling: Bio, Career, and Hollywood Connection Life with Tom Welling

Api Robin: The Quiet Force Supporting Celeste Barber

Linda Bazalaki — Life After the Crown, Miss Uganda 1993

Melanie Sergiev: The Woman Behind Drew Lynch’s Success Story

Vera Davich: The Enigmatic Life of Scott Patterson’s First Wife

Kamiri Gaulden: What You Should Know About NBA YoungBoy

Talia Elizabeth Jones: Her Life, Parents, and Connection to Davy Jones

How Newly Arrived Immigrants in the UK Can Stay Financially Compliant

Top Health Colleges in the Middle East in 2026

What Really Happens When Pet Food Passes Its Expiry Date

How Dry and Wet Pet Food Are Made and Why Ingredients Matter

Top Health Colleges in the Middle East in 2026

Tennis Chain Durability: Diamond Setting, Structural Strength, and Long-Term Wear

3 Steps to a Successful Quinceanera

Building Stronger Communities Through Corporate Partnerships

Understanding Professional Networks for Expert Knowledge

General Audience: Key Considerations When Evaluating Ai Orchestration by Ba Insight

-

Celebrity1 year ago

Celebrity1 year agoChristina Erika Carandini Lee: A Life of Grace, Heritage, and Privacy

-

Celebrity1 year ago

Celebrity1 year agoTrey Kulley Majors: The Untold Story of Lee Majors’ Son

-

Celebrity1 year ago

Celebrity1 year agoNick Schmit? The Man Behind Jonathan Capehart Success

-

Celebrity1 year ago

Celebrity1 year agoJamie White-Welling: Bio, Career, and Hollywood Connection Life with Tom Welling